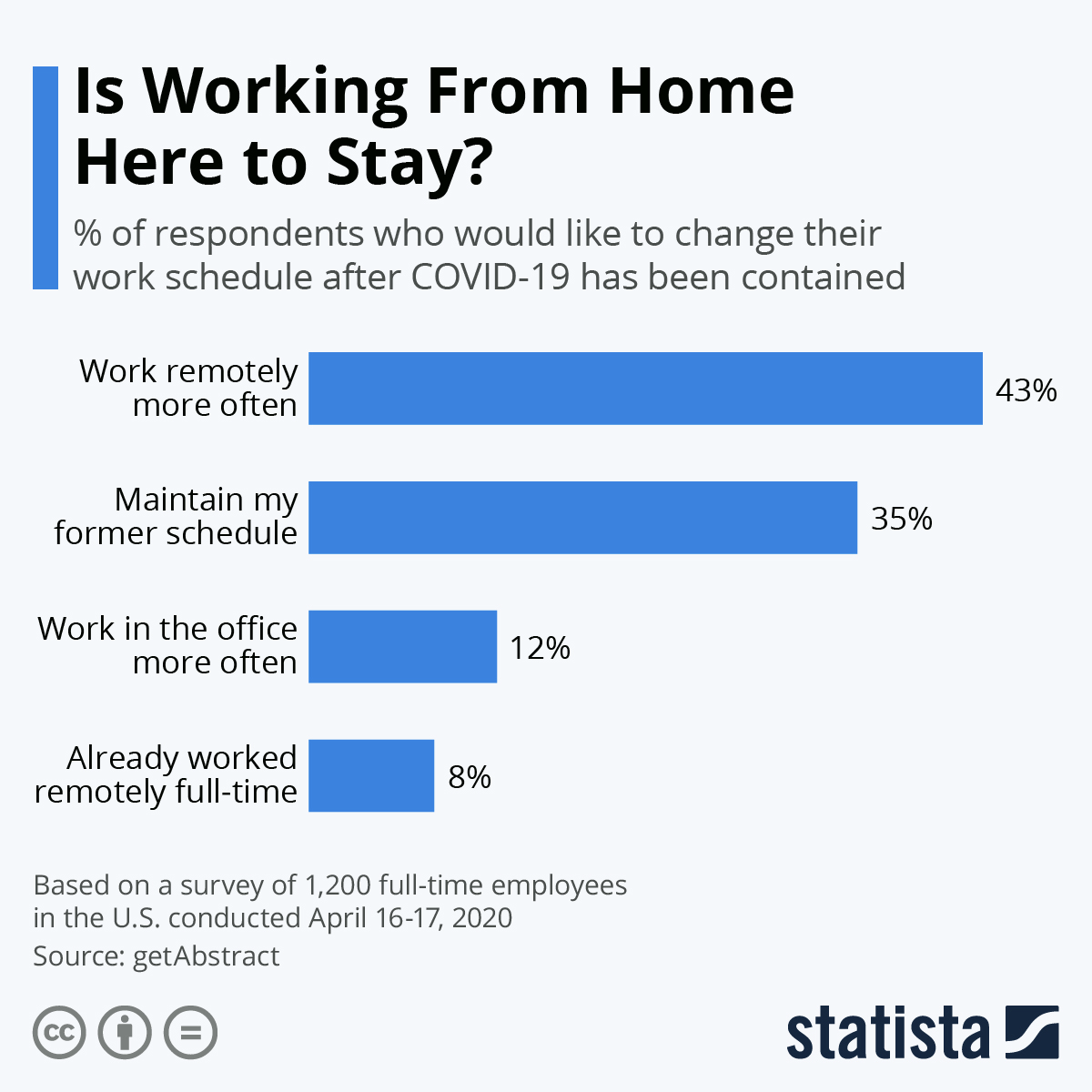

It goes without saying that many Americans transitioned to working from home for the first time due to the worldwide pandemic. Such a change in the way businesses and employers operate has led to a tricky question of public policy: how to tax businesses whose workers mostly operate from home.

The Ohio Legislature sought to answer this question at the start of the pandemic. On March 27, 2020, Ohio Gov. Mike DeWine signed into law a bill that prescribed a misguided solution.

House Bill 197 enables cities to collect municipal income taxes from commuters whose employers temporarily closed their downtown offices due to the pandemic.

The Buckeye Institute, a nonprofit, free market-oriented think tank based in Columbus, Ohio, has filed a notice of appeal with Ohio’s First District Court of Appeals in Schaad v. Alder, a case that challenges the city of Cincinnati’s application of local income tax to nonresident commuters who worked from home during the pandemic.

The suit seeks to prove the city’s emergency-based tax policy is unconstitutional, which I believe it objectively is.

As a result of the pandemic, workers who worked from home are having their labor treated as if it were performed in higher-taxed municipalities, meaning individuals like Josh Schaad (who spent less time in Cincinnati this past year for work) had to pay more in municipal income taxes in 2020 than in 2019.

Mr. Schaad had previously worked remotely and thus received subsequent refunds for work not conducted in Cincinnati. H.B. 197, though, outlawed such a common-sense solution.

Schaad v. Alder is just one of five cases the Buckeye Institute has pursued in protest of H.B. 197.

Denison v. Kilgore is strikingly similar to Schaad v. Alder in that Eric Denison worked offsite in Westerville, Ohio, yet had his labor taxed as work conducted in Columbus. Denison also was successfully reimbursed in prior years for work performed outside the city limits of Columbus, but as with Schaad, such a practice was prohibited by H.B. 197.

This past April, Franklin County settled the case and thus repaid Denison what he was owed in taxes. They also agreed to continue such practice, no longer requiring him to pay higher Columbus taxes in the future.

In a third case related to the bill, the Buckeye Institute on May 26 appealed the decision in Buckeye v. Kilgore, originally filed in July 2020. The case similarly asks the question of whether the work of employees who are forced to work from home should be treated as if it was performed in a different city for tax purposes.

In March, Buckeye filed a suit against the cities of Oregon and Toledo, Curcio v. Hufford, citing the Due Process clause of the U.S. Constitution as grounds for H.B. 197’s unconstitutionality. Beyond the legal reasons for why the law should not apply, in practice, the workers in question did not receive any tax-paid benefits or services from the cities of Oregon and Toledo, as they did not live there.

Why should any individual pay tax to a municipality in which they do not live and from which they do not receive any additional benefits or services?

The fifth case pursued by Buckeye pertaining to H.B. 197 was Morsy v. Dumas, filed in Cuyahoga County this past April. Dr. Manal Morsy lives in Pennsylvania but works in Cleveland.

Morsy had not stepped foot in Cleveland (or Ohio for that matter) since March 2020, but she had been paying income tax to the city of Cleveland, as well as her hometown of Blue Bell, Pennsylvania, more than 400 miles from Cleveland, for over a year.

Buckeye called such tax policy a “modern day form of taxation without representation.”

"commuters pay taxes without having a voice in city government. It’s taxation without representation" is exactly right. That is why Buckeye has filed cases across #Ohio. Read more about our cases: https://t.co/aIuPLoTiBe https://t.co/hKOJn1QDdV

— The Buckeye Institute (@TheBuckeyeInst) June 11, 2021

The issue of unjust tax policy during the pandemic is not unique to Ohio, however. An even more significant legal challenge to pandemic tax law is underway right here in New England.

Buckeye filed an amicus brief to the U.S. Supreme Court in New Hampshire v. Massachusetts, asking the court to protect Granite Staters from unconstitutional taxation by Massachusetts.

Citing the Due Process clause again, litigators have pointed out that Massachusetts has been unfairly taxing New Hampshire’s many commuters, over 80,000 of them, who switched to work from home since mid-October 2020.

The Supreme Court has not yet decided whether or not to rule on the case, but such a ruling could establish uniform work from home tax precedent across the nation.

Now, with more people working from home than ever before (which for some is here to stay, permanently), it would be a good idea for the court to hear New Hampshire’s case and establish tax precedent for the nation following the pandemic.

Regardless of the high court’s decision, during the added stress, financial and mental burden brought on by the pandemic and our government’s response to it, no individual should have to worry about additional taxation without representation.