The U.S. Treasury Department has permanently barred from the banking industry a former Quontic Bank mortgage officer who originated dozens of home loans for rural Maine properties that were later converted into illicit Chinese marijuana grow houses.

The Maine Wire was the first — and remains the only — media outlet to report on the financial schemes undergirding the Chinese cannabis empire that blossomed in Maine beginning in 2020, including Quontic Bank and the now defunct Money Tree Capital Markets.

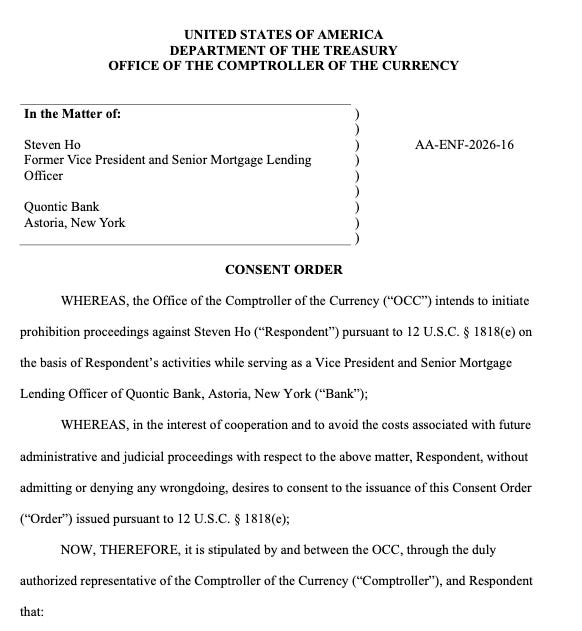

Steven Ho, who held the title of vice president and senior mortgage lending officer at Quontic Bank in Astoria, New York, agreed to a consent order issued by the Office of the Comptroller of the Currency, a bureau of the Treasury Department that charters and examines federal savings associations like Quontic. Ho signed the order on May 7. Leslie A. Chumbley, the OCC’s director for special supervision, made it final on May 18.

The order does what the federal banking laws call a prohibition: it bars Ho, for life, from participating “in any manner in the conduct of the affairs” of any insured bank, credit union, farm credit institution, or federal banking regulator. The ban lifts only if Ho someday obtains the written consent of both the OCC and the institution’s own regulator — a permission that is rarely sought and rarely granted.

Under the terms of the consent decree, Ho did not admit to any unethical or criminal actions whatsoever. Ho consented to the order “without admitting or denying any wrongdoing.”

Between July 2014 and January 2023, according to the order, Ho originated mortgages for Quontic, a self-described “adaptive digital bank.” During that time, the Comptroller found, Ho “worked with third-party mortgage brokers that were not approved in accordance with the Bank’s policy,” then “concealed his dealings with these brokers from Bank decisionmakers” and kept their involvement out of the bank’s mortgage system. The result, the order says, was that Quontic “generated inaccurate mortgage documentation, including loan estimates and closing disclosures, that did not disclose the role of the brokers or the associated fees.”

That was only the beginning. The OCC found that Ho “participated in the falsification of information contained in Uniform Residential Lending Applications,” the standard mortgage form known in the industry as a Form 1003. The falsified information, the order says, included “borrowers’ income, job titles, and employment history,” along with supporting documents such as “profit and loss statements, verifications of employment letters, and letters of explanation.”

In other words, OCC says the loan files were cooked.

Subscribe now to The Robinson Report…

The OCC determination adds a new perspective to what Ho, who was originally born in Taiwan, told me in a Jan. 2024 phone interview, when he bragged that Quontic’s mortgage profits increased by 1000 percent during Covid-19.

The order goes further. Ho, it says, “participated in the concealment of unemployment benefits from Bank decisionmakers in loan applications by directing borrowers to open new bank accounts, provide bank statements for other accounts, or delay submitting bank statements.” When obvious problems surfaced — “inconsistencies in borrower employment, income, and other related application documentation” — Ho “failed to escalate” them to the people at the bank who were supposed to be checking. And in perhaps the most damning single sentence in the document, the Comptroller found that Ho “guided borrowers and brokers on what to put in loan application documentation to avoid scrutiny from Bank decisionmakers.”

He was paid for it. The order states plainly that Ho “received commissions for loans closed, including those containing inaccurate information.”

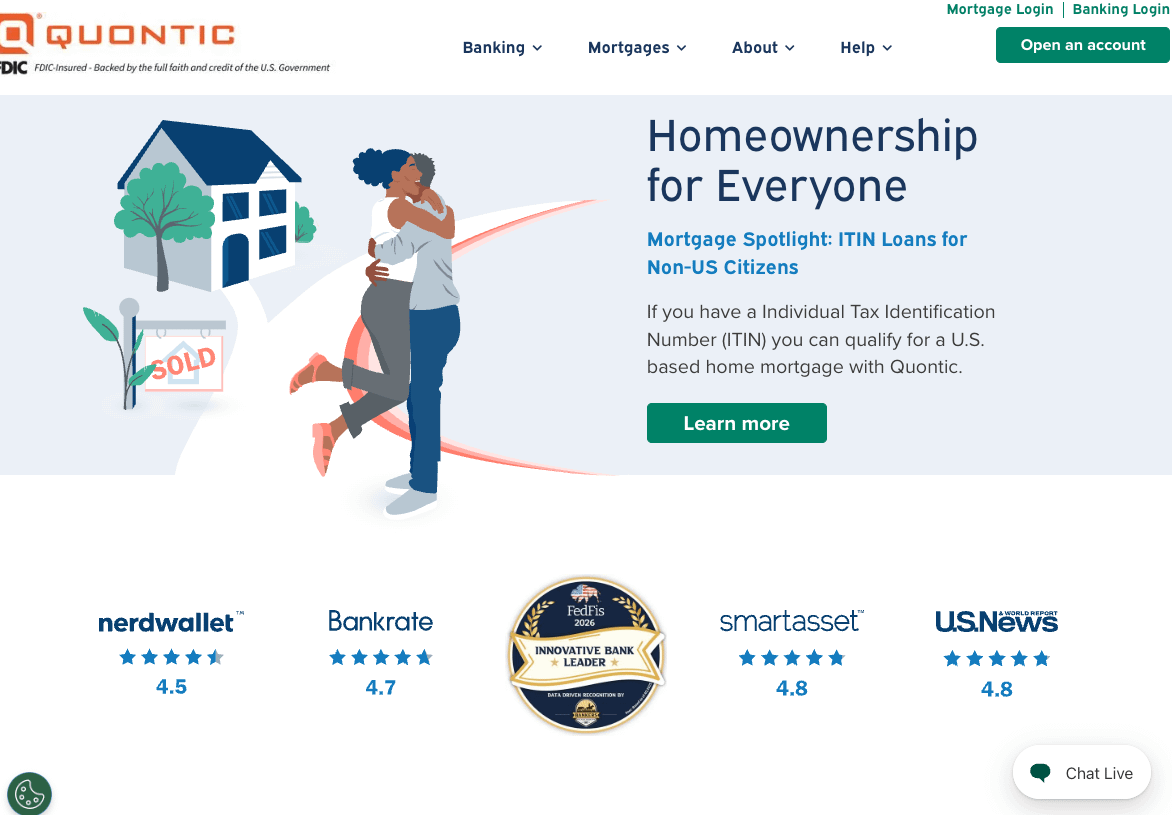

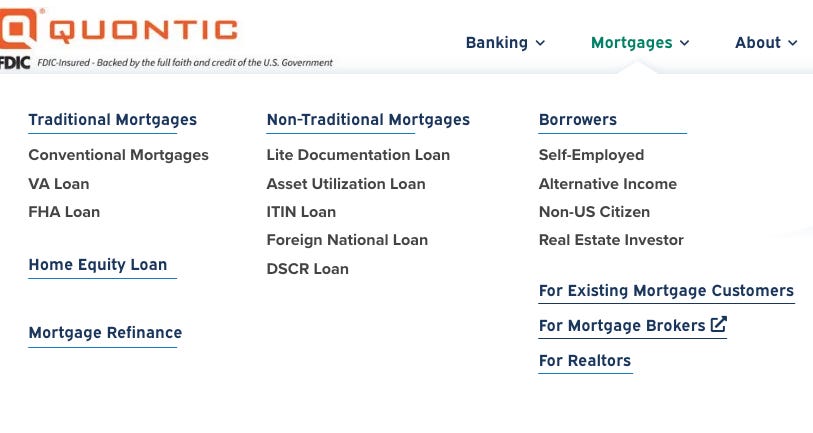

Critically, Quontic Bank is a financial institution that appeals specifically — if not exclusively — to foreign nationals looking to acquire property in the United States. Quontic’s website homepage currently touts mortgages for non-citizens, and the bank offers special loans for foreign nationals. Although the OCC consent decree does not say whether Ho’s alleged deception and fraud were aimed at helping foreigners acquire American houses and land, it seems likely given Quontic’s customer base and Ho’s own admission about his targeting of Chinese language communities.

According to the OCC, after Ho decided to leave Quontic to start his own mortgage venture, he raided the bank on his way out the door.

“Without approval from the Bank,” the order says, Ho “transferred, and was aware that other Bank employees transferred, confidential customer and business information of the Bank to support his new mortgage venture.”

That information was not trivial. It included, the order says, “the mortgage loan data for thousands of Bank customers such as the names, addresses, social security numbers, credit scores, and citizenship status of those Bank customers,” as well as the bank’s loan-investor information and its internal policies and procedures.

Ho shared all of it, the Comptroller found, “with non-Bank employees via unsecured email,” leaving the bank unable to give its own customers “clear and conspicuous notice” that their most sensitive data had been disclosed.

The OCC concluded that Ho’s conduct “resulted in inaccurate statements entered into the Bank’s books and records, concealed material information from Bank decisionmakers, and increased the Bank’s financial and other risks.”

By the agency’s reckoning, he “engaged in violations of law and regulation,” “breached his fiduciary duties to the Bank,” realized “financial gain or other benefit,” and “demonstrated personal dishonesty” — the legal triggers that allow a federal regulator to throw someone out of banking for good.

By signing the order, Ho waived his right to a hearing, his right to appeal, and his right to contest the order’s validity in any court. The settlement resolves the OCC’s own potential case against him, but it leaves every other door open. The agency reserved the right to use these same findings “in future enforcement actions to establish a pattern of misconduct,” and it made clear that nothing in the document limits “any other representatives of the United States or agencies thereof, including the Department of Justice, to bring other actions deemed appropriate.”

The OCC order never mentions Maine, marijuana, or illicit activity conducted by loan recipients. But both Quontic Bank and Ho played a significant role — unknowingly, Ho says — in securing financing for the sprawling network of Chinese cannabis grow houses in Maine. According to Maine deed registry records, more than 75 Chinese cannabis grows were financed using Quontic Bank. Almost half of those mortgages bear Steven Ho’s name as the mortgage officer. Those loans account for almost all of Quontic’s lending activity in Maine.

What the OCC describes — falsified incomes, manufactured employment letters, hidden unemployment checks, coached borrowers, and straw-buyer paperwork engineered to slip past the bank’s underwriters — is, almost line for line, the mechanism The Maine Wire began documenting in November 2023, when this outlet became the only news organization in the country to investigate Quontic Bank’s role in financing Maine’s Chinese organized-crime cannabis epidemic.

The pattern of behavior is precisely what would be beneficial to a transnational organized crime syndicate looking to rapidly acquire property in Maine for the purposes of cultivating and trafficking illicit cannabis.

In the phone interview, Ho said he did not know whether the loan documents OCC alleged contained fraudulent documents involved properties in Maine.

“I was not privy to those details,” said Ho.

All told, Quontic financed more than $15 million worth of residential mortgages for homes in rural Maine after 2020, despite having done almost no lending in the state before recreational cannabis was legalized here that year.

The two loan officers whose names appeared on the majority of those Maine files were Ho and his colleague Ying-Chan Weng, a Chinese national who attended Zhejiang University. In 2021, as the loans piled up, a mortgage-industry trade publication celebrated Ho’s “meteoric rise” under the headline “Top Originator: From a novice to a non-QM pro.”

Ho hinted that he disagreed with the OCC’s conclusions and that there was more to the story that he would not share based on the advice of his attorney.

“There’s unfortunately a lot more to it that I do not, I do not feel I can share that, you know, without speaking to counsel,” said Ho.

The properties Ho financed, according to mortgage documents filed with the various county deed registries, are scattered across the map of rural Maine.

One in Thorndike has been investigated as a suspected grow by the Waldo County Sheriff’s Office. According to the former sheriff, even the FBI had inquired about that property. One in Winterport caught fire because the marijuana operation inside was drawing too much electricity, leaving a family home gutted. Another in Rumford sits boarded up, reeking of cannabis, under investigation by local police.

Maine law enforcement — always sheriffs, never the Maine State Police — have also raided Quontic Bank-financed properties at 34 Clover Lane in Whitefield (owned by Hongxia Kuang), 9 Riverside Drive in Norridgewock (owned by Hai Bin Cen), 204 Rome Road in Mercer (owned by Yong Yuan Wu), 107 Perkins Street in Norridgewock (owned by Patrick Yam), and 555 Belfast Road in Freedom (owned by Austin Zhen).

WATCH: High Crimes: The Chinese Mafia’s Takeover of Rural America…

None of this would have been possible at scale without the federal program at the center of it. Quontic is a community development financial institution, or CDFI — a designation Congress created in 1994 to push banks to lend in underserved and immigrant communities, and one that comes wrapped in taxpayer support.

Quontic received its CDFI status in 2015.

Federal records show the bank collected more than $3 million in grants beginning in September 2020, money drawn from a $20 million “rapid response” tranche of CDFI funding rushed out during the pandemic, and that taxpayers subsidized 373 of its loans.

The CDFI rules also let Quontic do what conventional banks cannot: lend to borrowers who are not U.S. citizens, who cannot document regular income, and who source their down payments and closing costs from third parties — every one of which is a feature a transnational criminal organization looking to launder money into American real estate would find useful, and all of which Quontic advertised openly on its website.

There’s no evidence laid out in the consent decree that Quontic Bank was aware of the activity that would later occur at the properties they financed. And there’s never been any accusation of wrongdoing leveled against Quontic or any of its current leadership.

The bank was started by visionary Steven Schnall in 2009, but Schnall died in a random motorcycle accident while on his way back from a biking trip to Canada.

In a phone interview with The Maine Wire in January 2024, Ho was candid about how good the business had been and how he found his customers. He described targeting the Chinese-speaking community directly.

“My marketing is towards the Chinese community, and because I speak Chinese, so when someone comes to me for a loan and I help them based on, you know, what they can qualify for because of the community that they belong in,” Ho said.

“One person refers to another person,” he said.

He summed up the strategy with a fishing metaphor: “You go fish where the fish are.”

The fishing was lucrative. Ho recalled Quontic’s explosive growth in the year the Maine loans began.

“I remember, in one of the meetings, the company grew 1,000 percent, which was incredible,” he said. “It was, like, you know, some crazy number.” He added: “Some strategic thing was happening where everyone was getting the — the right people were being hired. There was just some kind of momentum that was happening in 2020.” He said the boom was national, not specific to Maine, and that he was simply taking applications wherever clients wanted to buy.

Ho told The Maine Wire he had no idea what his borrowers intended to do with the houses.

“Do they tell me what they use it for? No, they don’t,” he said. “If I had knew that, you know, what you’re just saying right now — that they wanted to use the property for non-legal purposes — I would not have taken their application.”

The OCC’s order does not accuse Ho of knowingly financing drug operations, and he has not been charged with any crime.

But the techniques the Comptroller attributes to him are the same ones federal prosecutors later put at the heart of the first bank-fraud case to come out of Maine’s cannabis epidemic.

In December 2024, a federal grand jury in Maine indicted Yuantong Liang, 36, and Yongliang Deng, 34, on charges tied to falsifying documents to secure mortgages for homes that became grow houses in Bucksport, Eddington, and Canaan — properties bought in 2020 with fraudulent loans totaling $542,000. Liang was accused of paying associates to pose as buyers; investigators said he and his wife once put up $55,000 for a down payment while keeping control of the account. Liang faced 15 counts, including bank fraud and money laundering.

The paperwork, in other words, was built exactly the way the OCC says Ho built his. However, the loans tied to Liang and Deng were not originated by Quontic.

Ho left Quontic in August 2022, shortly after the bank’s founder and chief executive, Schnall, died at age 55 — the visionary, as Ho described him, who had taken the company “to the next level.”

For now, the order stands as the first formal federal sanction against anyone tied to the Quontic loans that would, unbeknownst to Ho or Quontic, help transform dozens of Maine homes into drug factories.

Unknowingly my foot.

What about the others who facilitated the purchases, like Mills?

It looks to me like he’s a fall guy for a whole bunch of other people…

And our Governor had absolutely no idea this was going on…. Riiiiight.

Great reporting Steve. This is the tip of the iceberg

Mr. Ho has been reported to have had help from the lawyer bother of Maine’s Governess Ho. I believe it was the Maine Wire that reported that her Brother helped with the legal work on one or more of these Pot Houses. I believe that the Maine State Police are under the direct order of the Maine Governor. This excellent article by Mr. Robertson points out that the Maine State Police have not been involved in enforcement actions against the some 400 Chinese owned Pot Houses in our State.

Is it standard practice to give criminals the option to stop illegal activities & go away? I can’t understand why we have jails then. How does one sign up for this legal option? Asking for a friend!

This all took place under THE DEMOCRAT JOE BIDEN, Where were Maine Democratic leaders? Pingree, Her Daughter, King, The governor, and Attorney general.

And there is still no scientific evidence that grass has any Medical Value, just here say. Show me the proof. It is just mind control by the Dema.

Great reporting from the Maine Wire, AGAIN!!! Count down starts as to when Maine legacy media will steal this incredible investigative journalism and claim it as theirs!!!